My #1 Tip for Keeping Your Financial Self Care Sustainable

Self-care is important, but if you never actually do it, it’s not that valuable. The key to reaping the rewards from a financial self care routine is making sure it’s something you can actually do on a regular basis. So far this month, we’ve talked about the importance of financial self care. We’ve also touched on why regular “money time” makes a difference. Finally, last week, we focused on three simple steps you can take to infuse financial self care into your work routine. To wrap up this month’s series, let’s focus on how we can make sure you are able to keep that routine going sustainably.

Celebration

Yep, my number one tip for keeping your financial self care routine is celebration. Specifically, celebrating your financial wins. A financial win is any instance where you get a little bit closer to a goal you’ve set for yourself. So even if it’s just saving an extra $5, resisting the urge to spend on something small, paying down your debt just a bit, or making the first appointment with a bookkeeper or coach, these are big steps, and they deserve to be celebrated.

In my series on how to do a mid-year business review, I wrote this passage on celebrating your financial wins:

…[T]ake stock again of all you’ve done this year, including this review process. Chances are, you will find you’ve done quite a bit of work towards your goals, no matter how close you might be to completing them! Take some time to celebrate all the work you’ve done. Treat yourself to an afternoon off, a fun or inspiring event, or whatever you’d like to do to celebrate your achievements so far! Being a self-starting solopreneur is hard work. If you’ve done the work, you deserve to cheer yourself on once in a while.

I whole-heartedly believe this is true, and especially with the challenges this year has faced us with, we definitely need a moment to look at all our accomplishments and congratulate ourselves. Doing this is important to sustaining our financial self care routine, because it encourages to keep moving forward on our goals.

I invite you to find whatever feels like it would be the most meaningful way to celebrate these things. It might be sharing them with other people, like a money buddy or a mentor. It could be rewarding yourself with a purchase or some time off. If you use the Profit First system, it’s time for your quarterly profit distribution! Think about what you’d like to use it for. If you need some help thinking about the most meaningful way to celebrate, check out The Soul of Money by Lynne Twist.

Marking Time and Progress

Over the years, running your business may often feel like a blur. In order to get the fulfillment and satisfaction you want from it, it’s important to take time to mark time and progress. Notice how long you’ve been running your business. Make a practice of keeping track how you’ve grown and progressed as a business owner. Celebrating your financial wins is one excellent way to keep up with that practice.

Marking time and progress also helps you create a sense of momentum and purpose. This helps you keep coming back to your financial goals. When you notice how your actions are bringing you closer to certain achievements, it gets easier to show up every day and do the work you need to do.

Marking time and progress also helps you create a sense of momentum and purpose. This helps you keep coming back to your financial goals. When you notice how your actions are bringing you closer to certain achievements, it gets easier to show up every day and do the work you need to do.

So, celebrate yourself today! If you’d like more thoughts on celebrating your financial wins and other topics in the realm of financial self care, download my free e-Book, 9 Secrets to Financial Self Care.

Angela

Photo by Aaron Burden

with me if you want to know more about how the process might apply to you.

with me if you want to know more about how the process might apply to you.

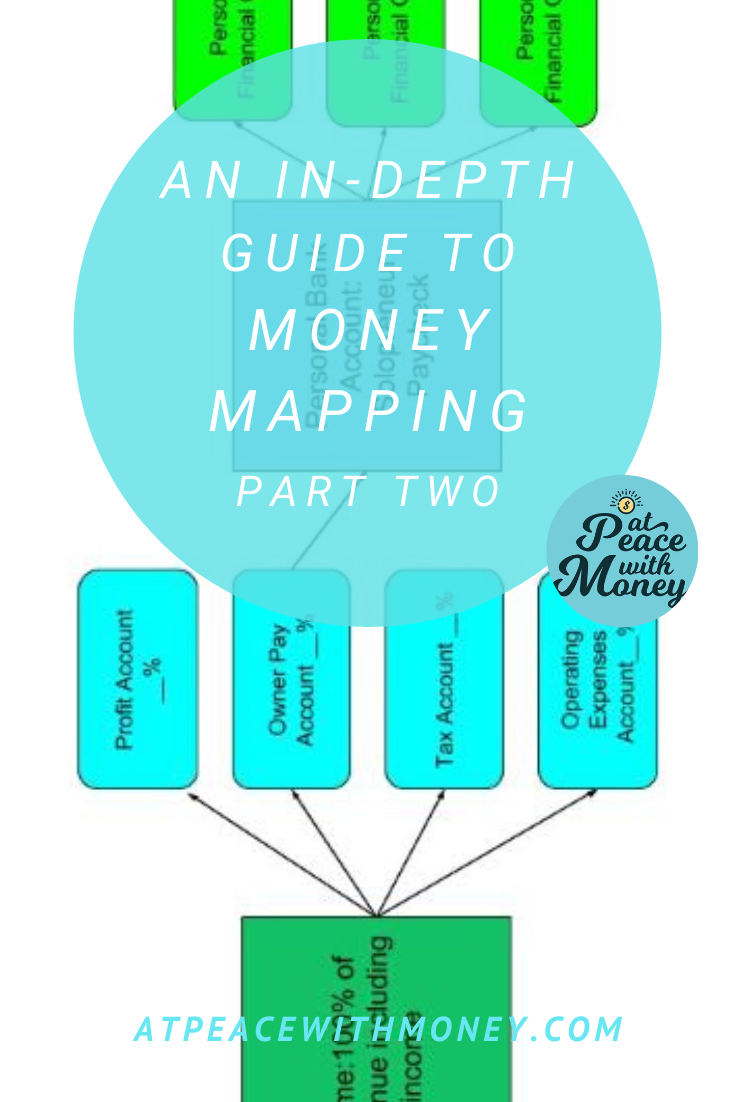

The Function of Profit

The Function of Profit

Above all, the goal of money mapping is to know where your money is going every step of the way. From the moment you receive income, to the moment that money is saved for taxes, invested for retirement, or put away for a savings goal – you’ve got a plan. Consequently, this is an opportunity to define those final destinations. Creating a tax savings account and an operating expenses account come in handy here. You can also think about creating savings goals for yourself, and making a plan to contribute regularly to those.

Above all, the goal of money mapping is to know where your money is going every step of the way. From the moment you receive income, to the moment that money is saved for taxes, invested for retirement, or put away for a savings goal – you’ve got a plan. Consequently, this is an opportunity to define those final destinations. Creating a tax savings account and an operating expenses account come in handy here. You can also think about creating savings goals for yourself, and making a plan to contribute regularly to those.

Doing some emotional work around money can also really help you clear up your oversaving. I recommend reading

Doing some emotional work around money can also really help you clear up your oversaving. I recommend reading

or for expansion. You can read more about the

or for expansion. You can read more about the

To solve this problem, I recommend two things. First, work with a tax preparer or bookkeeper who will help estimate a percentage to be held out for taxes. You can read more of my advice about working with a

To solve this problem, I recommend two things. First, work with a tax preparer or bookkeeper who will help estimate a percentage to be held out for taxes. You can read more of my advice about working with a

If you’ve already priced your products and wound up in a similar situation to the woman above, you can still double back and figure out your true income targets and prices. The real challenge comes in actually implementing a rate change. Before you do this, it can be helpful to

If you’ve already priced your products and wound up in a similar situation to the woman above, you can still double back and figure out your true income targets and prices. The real challenge comes in actually implementing a rate change. Before you do this, it can be helpful to

This is one of my favorite practices from the

This is one of my favorite practices from the

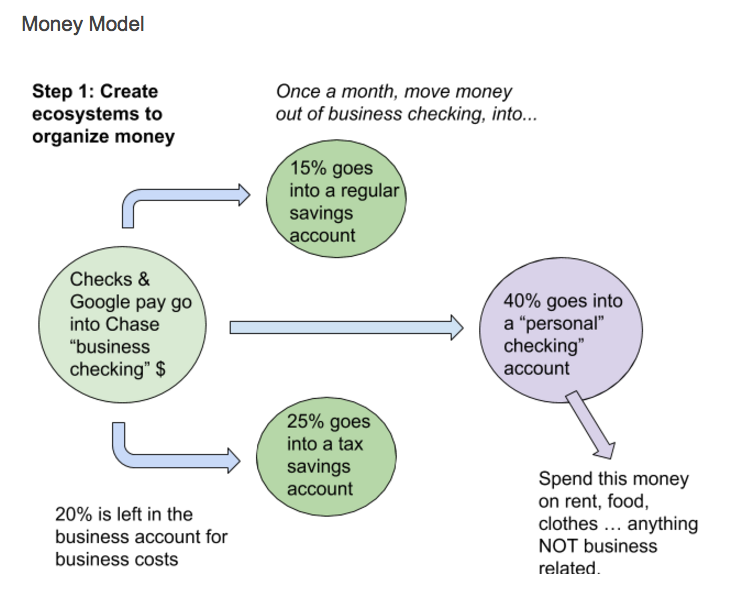

While you’re nailing down the banking details of your new business, make sure you also create a money system for yourself. Have a plan to pay off your expenses and also pay yourself. My recommendation, of course, is Profit First, which

While you’re nailing down the banking details of your new business, make sure you also create a money system for yourself. Have a plan to pay off your expenses and also pay yourself. My recommendation, of course, is Profit First, which